Gst Composition Scheme, Job Work, And Itc Rules Explained

The Goods and Services Tax (GST) has transformed India's indirect tax system into a unified, transparent, and business-friendly regime. If you

Small taxpayers with an annual turnover up to ₹50 lakhs can opt for the Composition Scheme. They pay tax at a flat rate of at least 1% of their total turnover and cannot claim input tax credit (ITC).

Eligibility restrictions:

Taxpayers making inter-state supplies or paying tax on a reverse charge basis are not eligible.

Only dealers and manufacturers can opt for it; service providers cannot.

A job worker is a person who processes raw materials or semi-finished goods supplied to them. This completes part or all of the manufacturing process, resulting in a finished article or performing any essential operation.

Key GST rules for job work:

Job workers must register under GST if their aggregate turnover exceeds the threshold limit.

Only registered principals can supply taxable goods to a job worker without paying tax.

Principals can send goods from one job worker to another.

Principal's turnover impact:

If the principal's goods are supplied directly from the job worker's premises, it counts toward the principal's turnover—provided the job worker is registered, and the principal declares the job worker's place as an additional place of business or notifies the goods movement.

For inputs or capital goods sent for job work:

The principal can claim ITC only if the goods are returned within 180 days from the date they were sent to the job worker.

If sent directly to the job worker, the 180-day clock starts from the date of receipt by the job worker.

Reversal rules:

If goods aren't returned on time, the principal must reverse the ITC availed (pay back the amount) plus interest.

ITC is restored once the goods are actually returned.

The Goods and Services Tax (GST) has transformed India's indirect tax system into a unified, transparent, and business-friendly regime. If you

Effective tax planning is essential for individuals and businesses to reduce their tax liabilities and ensure that they are in compliance with tax

Finding a reliable Chartered Accountant (CA) in Dwarka, Delhi, can be a game-changer for your business and personal finances. Whether you are a sta

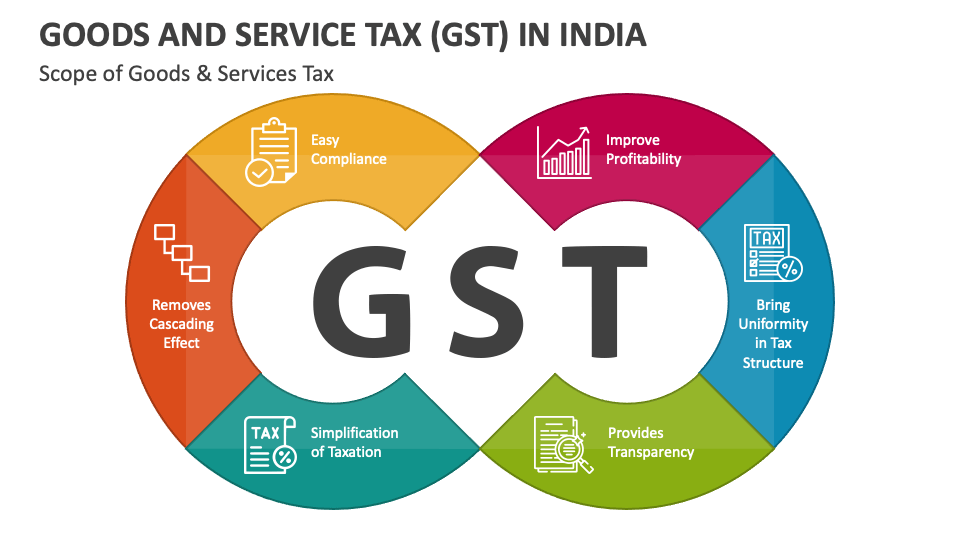

GST in India: Introduction, Law, and Taxation Goods and Services Tax (GST) is India’s unified indirect tax system that applies to the

Composition Scheme Small taxpayers with an annual turnover up to ₹50 lakhs can opt for the Composition Scheme. The

Goods and Services Tax, commonly known as GST, plays a major role in the tax compliance process for businesses in India. Filing GST returns correct

Starting a business in Dwarka? One of the first and most important steps is getting your GST Registration done. The Goods and Services Tax (GST) is

Filing your Income Tax Return (ITR) is an important financial responsibility. However, many individuals make small but crucial mistakes that can le

If you are looking for a reliable CA in Dwarka, Delhi, our team of experienced Chartered Accountants i

Gurgaon has become a startup hub, and with rapid business growth comes the need for reliable financial management. CA services in Gurgaon provide s

In today’s competitive business environment, hiring a CA in Gurgaon has become more than just a necessity—it is a growth strategy. Chartered ac

Since the introduction of Goods and Services Tax (GST), businesses across India have had to adapt to a new way of managing their tax responsibiliti

Managing taxes can feel overwhelming for many salaried professionals in Delhi. Every year, when the deadline for filing Income Tax Returns (ITR) ap

Any business organization that earns an annual gross revenue of more than 20 lakhs must apply for the GST registration process, as per the guidelin

Whenever there are value related errors, Debit and Credit Notes come into the picture. Whether it is an upward revision or a downward revision in p

Government imposes a tax on the taxable income of all the persons who are Individual, HUF, Company, firms, LLP, AOP, BOI, Local Authority and any o

There are many types of supply but these 4 have similarities and differences too.Due to the similarities in names there is a lot of confusion and p

Before we proceed further, let us know What is GST? It is GOODS AND SERVICE TAX , it is Indirect tax levied on Goods and Services.

A Company is an artificial person created by Law and having a separate existence of its own.In simple Words, It is a legal entity formed by a group

It means Electronic Way Bill. Let us understand its meaning and its characteristics. It is the document required for Movement of G

Refund is a very important term under the GST for the person who

In this article we will learn about….. What is GST Returns? Who should file, Due Dates and Types of GST Returns.

ITR Filing in Dwarka, CA Near me, Best ITR Consultant in Dwarka, ITR in Dwarka , ITR Consultants in Dwarka, ITR Procedure in Dwarka,

Net worth certificate is a document which shows financial worth of an individual or company certified by a Chartered Accountants.

As per Finance Act 2013,Section 194IA, Any person purchasing property more than Rs50 lac than person has to deduct 1% tds on property value, this s